Trade

Basic

Futures

Futures

Hundreds of contracts settled in USDT or BTC

TradFi

Gold

Trade global traditional assets with USDT in one place

Options

Hot

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Futures Kickoff

Get prepared for your futures trading

Futures Events

Participate in events to win generous rewards

Demo Trading

Use virtual funds to experience risk-free trading

Earn

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

Launchpad

Be early to the next big token project

Alpha Points

Trade on-chain assets and enjoy airdrop rewards!

Futures Points

Earn futures points and claim airdrop rewards

Investment

Simple Earn

Earn interests with idle tokens

Auto-Invest

Auto-invest on a regular basis

Dual Investment

Buy low and sell high to take profits from price fluctuations

Soft Staking

Earn rewards with flexible staking

Crypto Loan

0 Fees

Pledge one crypto to borrow another

Lending Center

One-stop lending hub

VIP Wealth Hub

Customized wealth management empowers your assets growth

Private Wealth Management

Customized asset management to grow your digital assets

Quant Fund

Top asset management team helps you profit without hassle

Staking

Stake cryptos to earn in PoS products

Smart Leverage

New

No forced liquidation before maturity, worry-free leveraged gains

GUSD Minting

Use USDT/USDC to mint GUSD for treasury-level yields

More

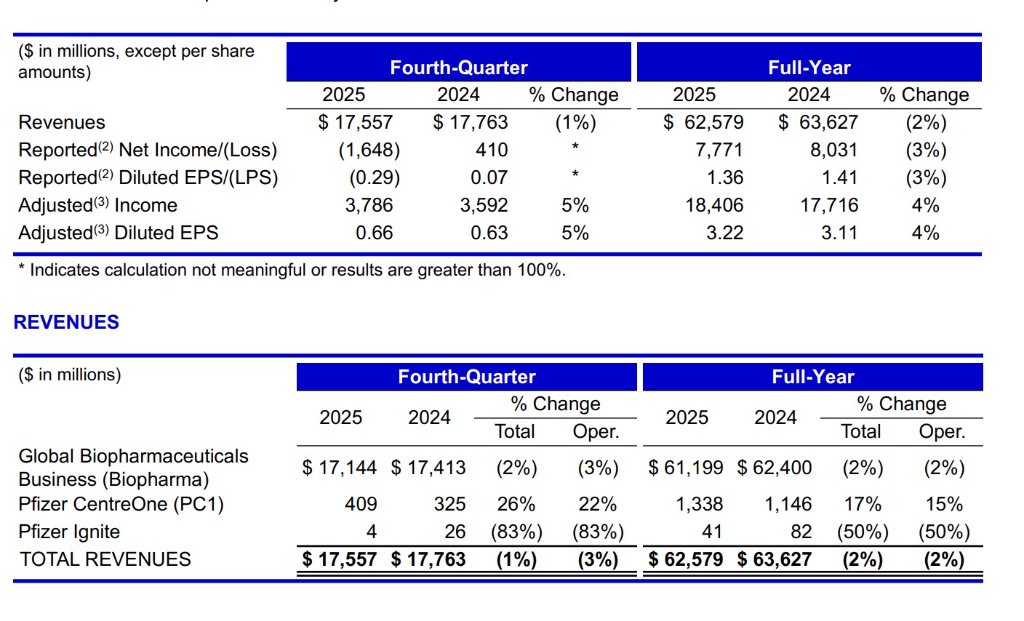

Pfizer's Q4 2025 revenue is $17.56 billion, with non-COVID business growing by 9%. The full-year revenue guidance for 2026 is $59.5 billion to $62.5 billion | Earnings report news

On February 3rd, Pfizer released its 2025 full-year financial report, demonstrating solid operational resilience during its strategic transformation phase.

The financial report shows that total annual revenue reached $62.6 billion, and after excluding COVID-related products, its core business portfolio achieved a 6% operating growth. Adjusted earnings per share (EPS) reached $3.22, up 4% year-over-year, reflecting the company’s continued strengthening profitability. Notably, Pfizer maintained its 2026 performance guidance while disclosing an active product pipeline advancement plan, with approximately 20 key clinical trials expected to launch by 2026, laying a foundation for long-term growth.

Looking at Q4 performance, revenue for the quarter was $17.6 billion; excluding COVID products, quarterly revenue increased by 9% year-over-year, further accelerating the growth rate compared to the full year. Adjusted EPS was $0.66, up 5% year-over-year, indicating ongoing optimization in cost control and operational efficiency. This “overall stability with a strengthening structure” characteristic precisely confirms that Pfizer is at a critical stage of transitioning from pandemic-related income to innovation-driven growth. CEO Albert Bourla stated that effective execution in 2025 has laid a solid foundation for Pfizer’s future growth, and 2026 will be an important year for the company to usher in multiple key catalysts. CFO David Denton also emphasized that by focusing on business execution and maintaining financial discipline, the company achieved strong EPS performance. Management’s confidence mainly stems from further clarification of strategic direction and the continuous enrichment and strengthening of the late-stage R&D pipeline.

CEO Albert Bourla stated that effective execution in 2025 has laid a solid foundation for Pfizer’s future growth, and 2026 will be an important year for the company to usher in multiple key catalysts. CFO David Denton also emphasized that by focusing on business execution and maintaining financial discipline, the company achieved strong EPS performance. Management’s confidence mainly stems from further clarification of strategic direction and the continuous enrichment and strengthening of the late-stage R&D pipeline.

Strong growth in non-COVID business, continuous optimization of product portfolio

In the full-year 2025 results, Pfizer’s non-COVID product portfolio demonstrated robust structural growth. Against the backdrop of a significant decline in COVID-related revenue, the company successfully transitioned its business focus toward innovative therapies through ongoing portfolio optimization and market share expansion.

Cardiovascular and vaccine segments lead growth. The anticoagulant Eliquis achieved $8 billion in annual revenue, up 8%, becoming the company’s second-largest product, mainly benefiting from improved healthcare reimbursement environments in the U.S. and steady global demand. The Prevnar vaccine series generated $6.5 billion in revenue, up 1%, with notable performance in adult indications in international markets.

The Vyndaqel family of cardiac disease treatments was a highlight of the year, with revenue up 17% to $6.4 billion, driven mainly by increased diagnosis rates and improved payment conditions in the U.S. Despite some pricing pressures in Q4, this product still achieved $1.7 billion in revenue, up 9%, maintaining strong growth momentum.

Rapid volume growth of innovative products. The RSV vaccine Abrysvo surpassed $1 billion in revenue in its second year on the market, with a 37% increase. The product quickly penetrated international markets among adults and pregnant women. Although U.S. market adjustments based on public health agency recommendations impacted sales, overall growth remained high, with Q4 revenue soaring 136% year-over-year to $481 million.

The migraine treatment Nurtec ODT/Vydura grew revenue by 13% to $1.4 billion, further consolidating its market position in its niche segment.

Robust growth in oncology, ongoing pipeline value release

Pfizer’s oncology segment achieved $16.8 billion in revenue in 2025, up 8%, with operating growth matching this increase, making it the most stable among the company’s three major business units.

Core products maintain market position. Despite competition from generics, breast cancer drug Ibrance contributed $4.1 billion, down 6% YoY, but still remains a pillar in the oncology portfolio. Prostate cancer drug Xtandi grew 8% to $2.2 billion, mainly benefiting from increased demand in the U.S.

Next-generation therapies show strong growth momentum. The antibody-drug conjugate Padcev (for bladder cancer) achieved $1.9 billion in revenue, up 22%, demonstrating the commercial potential of ADC technology. Lung cancer treatment Lorbrena surpassed $1 billion, with a 40% increase YoY, with market share in ALK-positive non-small cell lung cancer (NSCLC) continuing to rise.

Biosimilar business provides stable growth. The oncology biosimilar segment generated $1.3 billion in revenue, up 25%, with a remarkable 76% growth in Q4, mainly due to favorable pricing environments in the U.S. This segment provides important cash flow support and stability for the company’s oncology operations.

COVID products meet expectations, contribution declines significantly

As expected by the market, Pfizer’s COVID-related products continued a significant decline in 2025. The COVID vaccine Comirnaty generated $4.4 billion, down 18% YoY; oral antiviral Paxlovid brought in $2.4 billion, down 59%. Together, these contributed approximately $6.7 billion, a sharp decrease from $11.1 billion in 2024.

Q4 performance was even more pronounced: Comirnaty revenue was $2.3 billion, down 35%; Paxlovid revenue was only $218 million, down 70% YoY. The decline was mainly due to reduced global COVID infection levels, adjustments in U.S. vaccination recommendations, and decreased international government procurement.

Notably, the company’s 2026 outlook estimates COVID-related product revenue at about $5 billion. This indicates that the business has largely transitioned from the pandemic phase to an endemic phase, continuing to provide relatively stable seasonal revenue.

Operational efficiency continues to improve, profit margins remain robust

Pfizer demonstrated excellent cost control in 2025. The full-year adjusted gross margin decreased to 24.2%, down 1.6 percentage points from 25.8% in 2024, mainly due to portfolio optimization of high-value products and increased manufacturing efficiency.

Cost structure optimization continues. Adjusted selling, general, and administrative (SG&A) expenses totaled $13.6 billion, down 7% YoY, further reducing their proportion of revenue. The company focused on core product promotion and digital capabilities to achieve precise and efficient marketing resource allocation.

Adjusted R&D expenses were $10.2 billion, down 5%, but this does not mean R&D investment shrank. Through pipeline optimization and digital tools, the company maintained R&D intensity while significantly improving capital efficiency. In 2025, Pfizer launched 11 key clinical trials and plans to initiate about 20 in 2026, indicating ongoing improvements in R&D productivity.

The full-year adjusted effective tax rate was 12.7%, further down from 14.5% in 2024, mainly due to regional tax structure optimization and effective tax planning measures, creating additional value for shareholders.

In capital allocation, the company paid $9.8 billion in dividends to shareholders in 2025, with a dividend per share of $1.72, continuing its commitment to shareholder returns. Additionally, $10.4 billion was invested in internal R&D, with approximately $8.8 billion allocated to business expansion and related transactions, reflecting strategic investments in future growth areas.

Major acquisitions and pipeline progress, obesity treatment pipeline layout

Through strategic acquisitions and external collaborations, Pfizer is accelerating its layout in obesity and metabolic disease treatments. In November 2025, the company completed the acquisition of Metsera, with a total deal value of about $7 billion, including a contingent value right of up to $20.65 per share. This transaction provided Pfizer with next-generation obesity and cardiometabolic disease R&D pipelines, marking its official entry into this high-growth therapeutic area.

Rapid progress in obesity pipeline. In February 2026, Pfizer announced positive Phase 2b results for its ultra-long-acting GLP-1 receptor agonist PF-3944 (MET-097i). The study met its primary endpoint, achieving statistically significant weight loss over 28 weeks, with good tolerability. Notably, patients maintained weight loss trends after switching from weekly to monthly dosing, with no plateau observed.

Additionally, Pfizer reached an exclusive global partnership with YaoPharma for the development and commercialization rights of the small-molecule GLP-1 receptor agonist YP05002. Currently in Phase 1 trials for chronic weight management, the agreement includes a $150 million upfront payment and milestone payments up to $1.935 billion.

These initiatives highlight Pfizer’s strategic investments in obesity treatment. Among the approximately 20 key clinical trials planned for 2026, 10 will focus on assets acquired from Metsera, and 4 will target the PD-1×VEGF bispecific antibody PF-08634404, demonstrating clear R&D resource allocation and disease area focus.

Tumor pipeline achieves multiple regulatory breakthroughs

Pfizer’s oncology pipeline has made key clinical advances across multiple indications, further strengthening its product portfolio’s market competitiveness and therapeutic potential.

Padcev continues expansion in bladder cancer. In November 2025, the FDA approved the antibody-drug conjugate Padcev combined with pembrolizumab for perioperative treatment of muscle-invasive bladder cancer (MIBC) patients ineligible for cisplatin-based chemotherapy, based on positive Phase 3 EV-303 trial data.

In December 2025, the company announced interim results from the EV-304 (KEYNOTE-B15) study. This trial evaluated Padcev combined with pembrolizumab versus standard neoadjuvant chemotherapy in cisplatin-eligible patients, showing achievement of both primary endpoints: event-free survival and overall survival, laying a crucial foundation for expanding indications.

Tukysa maintains significant clinical value. According to Phase 3 HER2CLIMB-05 trial data, Tukysa combined with trastuzumab and pertuzumab as first-line maintenance therapy for HER2-positive metastatic breast cancer significantly reduced the risk of disease progression or death by 35.9%, supporting its leading role in this treatment area.

Braftovi shows outstanding performance in colorectal cancer. The January 2026 release of the BREAKWATER study Cohort 3 data indicated that Braftovi combined with cetuximab and FOLFIRI in BRAF V600E-mutant metastatic colorectal cancer achieved an objective response rate of 64.4%, significantly higher than the 39.2% in the standard therapy group, demonstrating superior clinical activity.

Projected full-year revenue in the range of $59.5 billion to $62.5 billion

The company fully confirms its 2026 financial guidance: projected full-year revenue between $59.5 billion and $62.5 billion, with adjusted EPS expected to be between $2.80 and $3.00.

The 2026 revenue guidance already includes approximately $5 billion from COVID-related products and accounts for about $1.5 billion in negative impact from patent expirations. The company expects full-year adjusted sales and administrative expenses to be approximately $12.5 billion to $13.5 billion, R&D expenses to be $10.5 billion to $11.5 billion, and an adjusted effective tax rate of about 15%.

This guidance considers current pricing policies (including “Most Favored Nation” pricing and TrumpRx drug pricing mechanisms) and the potential impact of tariffs already in place, but does not include possible future tariffs. These conservative assumptions provide buffer space for achieving performance targets.

The company explicitly states that it does not plan to conduct share repurchases in 2026 and will continue to focus on reducing debt levels and maintaining a balanced capital structure. This decision reflects management’s emphasis on financial robustness and preserves financial flexibility for future business development and strategic investments.

Risk Warning and Disclaimer