Stablecoins have emerged as a vital link between traditional finance and the blockchain economy. From digital asset trading and cross-border payments to on-chain financial applications, most stablecoins follow a similar lifecycle: assets enter a reserve system, tokens are issued, users circulate them, and they are ultimately redeemed back into fiat currency.

In the open stablecoin space, CASH represents a new frontier. Beyond maintaining a U.S. dollar peg and payment capabilities, CASH aims to connect developers, wallets, and payment platforms through an open ecosystem model. Unlike traditional stablecoins that focus primarily on issuance volume, CASH prioritizes continuous circulation and ecosystem expansion.

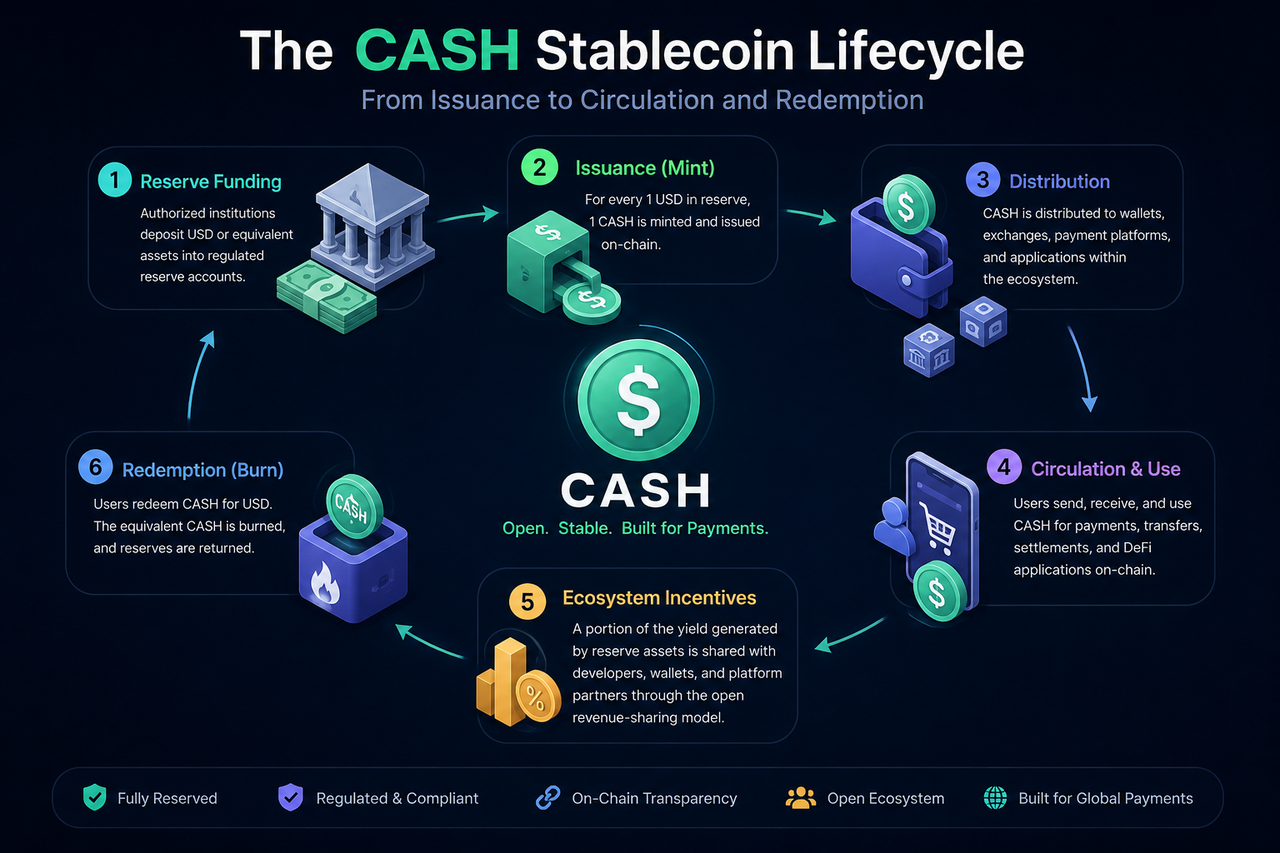

What Is the CASH Lifecycle?

The CASH lifecycle covers the complete journey from creation, entry into the market, participation in payments and transfers, to eventual redemption and destruction.

The process typically includes five key stages:

- Reserve assets enter custody;

- CASH is minted and launched on-chain;

- Users hold and transact with CASH;

- CASH circulates across payment and financial use cases;

- CASH is redeemed and burned.

This structure ensures that every CASH in circulation remains fully backed by corresponding reserve assets, preserving the stablecoin's value stability.

What Backs CASH Issuance?

CASH is a fiat-backed stablecoin.

The core principle of fiat-backed stablecoins is that each unit issued is supported by an equivalent amount of U.S. dollars or comparable assets. Reserves are held and managed by regulated custodians to ensure solvency.

This model mirrors cash deposits and bank accounts. Users holding CASH effectively own a digital claim on a proportional share of the reserve pool, rather than relying on algorithmic pricing or over-collateralization.

Thus, reserve management is the starting point of the CASH lifecycle.

How Does Bridge Enable CASH Issuance?

Bridge is a key infrastructure provider in the CASH ecosystem, responsible for the stablecoin issuance framework and fund settlement system.

When qualified institutions deposit U.S. dollars into the reserve, the system generates an equivalent amount of CASH based on the assets received.

For example, a $1 million deposit triggers the creation of 1 million CASH at a 1:1 ratio, which are then sent to designated wallets or platform accounts.

This process is called "minting." Once minting is complete, newly issued CASH enters the circulating market.

How Do Reserve Assets Support CASH's Value?

Reserve assets are the bedrock of CASH's stability.

Each CASH token is backed by a proportionate share of reserves, which typically include cash, short-term U.S. Treasuries, and other highly liquid, low-risk assets.

When market participants hold CASH, they are holding a digital representation of those underlying reserves.

Because reserves are highly liquid, redemption requests can be processed swiftly, helping CASH maintain its peg to the U.S. dollar.

How Does CASH Reach Users?

Once minted, stablecoins do not automatically land in users' wallets. Distribution occurs through the ecosystem network.

In the CASH ecosystem, wallets, payment platforms, and developer applications serve as key distribution channels.

Users can acquire CASH through:

- Converting U.S. dollars to CASH;

- Receiving transfers from others;

- Receiving funds as payment settlement;

- Obtaining balances from CASH-supported applications;

- Receiving earnings from on-chain financial activities.

This stage determines the stablecoin's circulation scale and user reach.

What Role Does Phantom Play in CASH Circulation?

Phantom, a major wallet infrastructure on Solana, serves as a key entry point to the CASH ecosystem.

When users manage assets through a CASH-compatible wallet, Phantom provides account management, asset display, and transaction signing.

Wallets do more than store stablecoins—they act as user gateways connecting payments, transfers, and dApp ecosystems.

As digital wallets evolve into comprehensive financial accounts, the deep integration of stablecoins and wallets is becoming an industry trend.

How Does CASH Facilitate Payments and Transfers?

Once users hold CASH, the stablecoin enters active circulation.

Users can send CASH to other addresses via the blockchain, or use CASH-supported payment systems for purchases and settlements.

Compared to traditional bank transfers, on-chain payments offer distinct advantages:

| Aspect |

CASH Transfer |

Traditional Bank Transfer |

| Settlement |

On-chain, real-time |

Bank clearing system |

| Availability |

24/7, always-on |

Limited by business hours |

| Cross-border |

Global, unified network |

Relies on international clearing systems |

| Programmable |

Supports smart contracts |

Limited functionality |

These features position stablecoins as critical infrastructure for internet-native payments.

How Does the Open Yield Mechanism Work in the Lifecycle?

Traditional stablecoin lifecycles focus on issuance, circulation, and redemption.

CASH adds an open revenue-sharing layer.

Reserve assets generate yield (e.g., interest from short-term Treasuries). In conventional models, this yield goes to the issuing entity.

Under the CASH model, a portion of that yield is distributed to ecosystem partners—developers, wallet providers, and payment platforms—according to predefined rules.

Thus, the CASH lifecycle reflects not only capital flows but also value distribution.

How Does CASH Handle Redemption and Destruction?

Users can redeem CASH for U.S. dollars by initiating a redemption request.

Upon completion, the system performs two actions:

First, it removes the corresponding amount of CASH from circulation.

Second, it releases the equivalent reserve assets and pays the user.

This process is called "burning."

The burn mechanism ensures that the circulating supply of CASH remains exactly aligned with reserve assets, preserving the stablecoin's integrity.

How Does CASH Differ from Traditional Stablecoin Issuance?

Technically, CASH operates similarly to fiat-backed stablecoins like USDC.

Both rely on asset reserves and manage supply through minting and burning.

The key difference lies in ecosystem design.

| Aspect |

CASH |

Traditional Stablecoins |

| Reserve-backed |

Yes |

Yes |

| Minting mechanism |

Yes |

Yes |

| Burning mechanism |

Yes |

Yes |

| Yield distribution |

Ecosystem shared |

Issuer centralized |

| Developer incentives |

Emphasizes open participation |

Relatively limited |

| Network expansion |

Partner-driven |

Issuer-driven |

CASH's innovation is not in issuance technology, but in the openness of its economic model.

Conclusion

The CASH lifecycle spans reserve custody, token minting, ecosystem distribution, on-chain circulation, payment applications, and eventual redemption and destruction. Its underlying logic mirrors mainstream fiat-backed stablecoins: reserve assets maintain the U.S. dollar peg, and minting/burning regulate supply.

What sets CASH apart is its emphasis on open ecosystems and revenue sharing. Beyond digital dollar issuance and payments, CASH seeks to build a scalable payment network through developer incentives and partner participation. This open stablecoin model is emerging as a new frontier in stablecoin infrastructure development.

FAQs

How is CASH minted?

CASH is issued through a fiat-backed mechanism. When corresponding U.S. dollar assets enter the reserve, the system mints an equivalent amount of CASH at a 1:1 ratio and releases it to the market.

Why does CASH maintain a stable value?

CASH is backed by reserve assets, and its supply is managed via issuance and redemption to maintain alignment with reserves, preserving its peg to the U.S. dollar.

Is CASH's issuance process the same as USDC?

Both use a fiat-backed model and manage supply through minting and burning. The difference is that CASH incorporates an open revenue-sharing mechanism.

How can users obtain CASH?

Users can acquire CASH by exchanging U.S. dollars, receiving transfers, settling payments, or using CASH-supported apps and wallets.

What is the CASH redemption process?

When a user requests redemption, the corresponding amount of CASH is burned, and the reserve system releases equivalent U.S. dollar assets to complete the refund.