As the BTCFi (Bitcoin DeFi) concept steadily gains momentum, the market is once again turning its attention to Bitcoin’s on-chain financial capabilities. Historically, Bitcoin was primarily viewed as a store of value, lacking the mature DeFi infrastructure seen on other networks. In recent years, however, the emergence of technologies such as Stacks, sBTC, and BitVM has endowed Bitcoin with stronger smart contract and asset expansion capabilities.

Zest Protocol is one of the BTCFi protocols born from this trend. It aims to build a lending marketplace that stays close to Bitcoin’s native ecosystem while providing foundational infrastructure for the future Bitcoin Layer2 financial system.

What Is the Background of Zest Protocol?

Bitcoin has long been the highest market cap digital asset in crypto, yet its on-chain financial ecosystem has developed relatively slowly compared to Ethereum. Ethereum rapidly built out lending, DEX, stablecoin, and derivatives markets via smart contracts, while Bitcoin largely remained a store of value and on-chain settlement layer. This has left vast amounts of BTC in a persistent low-utilization state.

BTCFi emerged to change this. BTCFi (Bitcoin DeFi) refers to the decentralized finance ecosystem built around Bitcoin, designed to offer BTC more on-chain financial applications while preserving Bitcoin’s security and decentralization. With the rise of Layer2 solutions, cross-chain bridges, and Bitcoin smart contract proposals, a growing number of protocols are exploring BTC lending, BTC yield assets, and native Bitcoin stablecoin marketplaces.

Zest Protocol positions itself precisely as the lending infrastructure for Bitcoin DeFi. Its core focus areas include:

- BTC collateralized lending

- Native BTC yield marketplace

- Bitcoin Layer2 financial protocols

- BTCFi liquidity infrastructure

- BTC credit marketplace for institutions and retail investors

In May 2024, Zest completed a $3.5 million seed round led by Tim Draper, with participation from Binance Labs, Flow Traders, Trust Machines, and others.

How Does Zest Protocol Work?

Zest Protocol uses an over-collateralized lending model, similar to Aave and MakerDAO in Ethereum DeFi, but its asset structure and underlying environment are more aligned with the Bitcoin ecosystem.

Users first deposit assets such as BTC, sBTC, or STX into the protocol as collateral. The system then calculates a user’s maximum borrowable amount based on the collateral ratio. Borrowers can lend stablecoins or other assets, while depositors earn returns through the protocol's interest rate.

The process is broken down into the following key components:

| Feature |

Role |

| Collateral asset deposit |

Users supply BTC, sBTC, STX, etc. |

| Lending marketplace |

System calculates Interest Rate based on liquidity |

| Liquidation mechanism |

Triggers risk liquidation when collateral ratio falls below threshold |

| Return distribution |

Depositors earn interest from lending activities |

| Smart contract execution |

On-chain logic executed via the Stacks network |

Unlike Ethereum DeFi, Bitcoin’s native network does not support complex smart contracts. Therefore, Zest Protocol implements its on-chain lending logic primarily through the Stacks network, using assets like sBTC to extend Bitcoin’s financial capabilities.

What Role Do Stacks and sBTC Play in Zest Protocol?

Stacks is a Layer2 network built on top of Bitcoin that enables developers to run smart contracts and decentralized applications while leveraging Bitcoin’s security. Most of Zest Protocol’s lending logic relies on Stacks for execution.

sBTC is a Bitcoin-pegged asset within the Stacks ecosystem, designed to allow BTC to participate in smart contract interaction while maintaining a 1:1 peg to Bitcoin. Through sBTC, users can bring Bitcoin liquidity into the Zest Protocol lending marketplace.

The combination of Stacks and sBTC allows native Bitcoin assets to enter DeFi scenarios, with Zest Protocol serving as a key financial application layer for these assets.

Currently, Bitcoin Layer2 and BTCFi are still in their early stages. However, with the Nakamoto Upgrade and the launch of more Bitcoin smart contract solutions, the BTCFi infrastructure is gradually maturing.

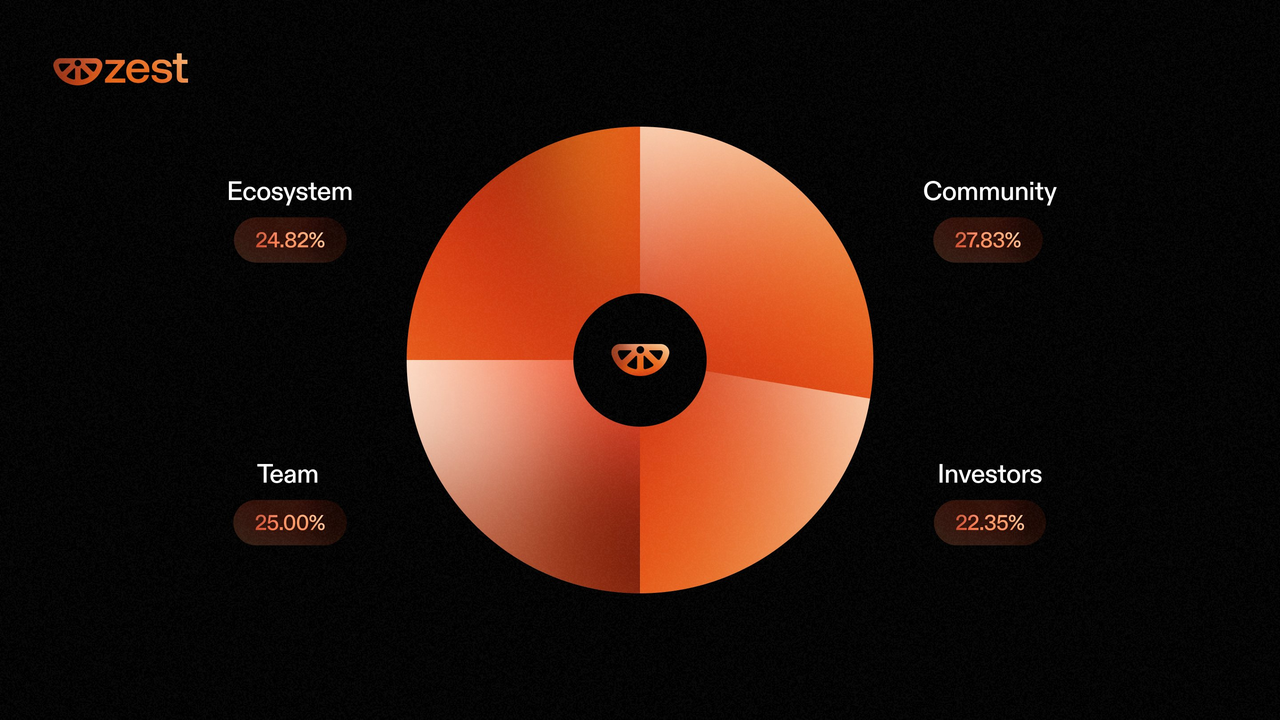

Zest Protocol tokenomics

Zest Protocol tokenomics

What Core Products Does Zest Protocol Support?

Zest Protocol is more than a single lending protocol—its ecosystem includes several BTCFi-related products.

BTC Borrow Market

The BTC Borrow Market is Zest’s core lending product, allowing users to lend stablecoins by collateralizing BTC and sBTC, thereby improving capital efficiency for BTC holders.

BTCz Yield Asset

BTCz is a yield-bearing BTC asset launched by Zest, designed to provide on-chain sources of return while maintaining BTC exposure.

Bitcoin Collateral Vaults

Bitcoin Collateral Vaults represent a key area of development for Zest. The goal is to enable native Bitcoin collateralized lending without relying on traditional Wrapped BTC custody models.

This structure aims to reduce bridge risk and enhance the security of Bitcoin’s native financial marketplace.

What Is the Difference Between Zest Protocol and Aave?

Both Zest Protocol and Aave are decentralized lending protocols, but their underlying ecosystems and asset structures differ significantly.

| Comparison Dimension |

Zest Protocol |

Aave |

| Core ecosystem |

Bitcoin / Stacks |

Ethereum |

| Core assets |

BTC, sBTC |

ETH, USDC, etc. |

| Smart Contract environment |

Bitcoin Layer2 |

Ethereum EVM |

| Primary goal |

BTCFi lending |

General DeFi lending |

| Development stage |

Early-stage BTCFi |

Mature DeFi |

Ethereum DeFi boasts a well-established liquidity and application ecosystem, while BTCFi is still in the infrastructure-building phase. As a result, Zest Protocol takes on the role of a pioneer in building Bitcoin’s native financial marketplace.

What Risks Does Zest Protocol Face?

As BTCFi remains an emerging space, Zest Protocol is exposed to several potential risks.

Smart Contract Risk

While Stacks smart contracts emphasize security, all on-chain protocols carry inherent vulnerability or attack risks.

Liquidity Risk

Compared to Ethereum DeFi, Bitcoin Layer2 liquidity is still relatively small, which could impact lending efficiency and market depth.

Liquidation Risk

Sharp movements in BTC's market price may trigger forced liquidation of user collateral positions.

Cross-Chain and Custody Risk

Some BTCFi structures still rely on bridged assets and cross-chain mechanisms, introducing potential custody and bridge security issues.

Regulatory Uncertainty

As global regulators intensify their focus on DeFi and stablecoins, BTCFi protocols may face new compliance requirements in the future.

Why Is BTCFi Attracting Market Attention?

Bitcoin has long commanded a massive AUM, but its on-chain financial activity has remained limited. The core thesis of BTCFi is to enable BTC not only to serve as a store of value but also to participate in lending, yield generation, liquidity provision, and stablecoin marketplaces—much like ETH.

This trend suggests that the Bitcoin ecosystem may evolve from “digital gold” into a full-fledged on-chain financial system.

BTCFi protocols, including Zest Protocol, are working to establish:

- A native Bitcoin lending marketplace

- A BTC stablecoin system

- BTC yield assets

- Bitcoin Layer2 financial infrastructure

- A native BTC collateral model

As more capital and developers enter the BTCFi space, competition in the Bitcoin DeFi marketplace is intensifying.

Summary

Zest Protocol is a decentralized lending protocol within the Bitcoin DeFi ecosystem that expands Bitcoin’s financial capabilities primarily through the Stacks network and the sBTC asset. Its goal is to allow BTC to participate in lending, yield generation, and on-chain liquidity marketplaces while preserving Bitcoin’s security.

As the BTCFi concept continues to develop rapidly, more protocols are exploring Bitcoin-native financial infrastructure, and Zest Protocol stands out as a key lending protocol among them. Although BTCFi remains early-stage, the advancement of Bitcoin Layer2 solutions, sBTC, and native BTC collateral models is driving Bitcoin’s transformation from a pure store of value into a productive asset capable of on-chain financial activity.

FAQs

Does Zest Protocol support native BTC?

Zest Protocol is advancing structures like Bitcoin Collateral Vaults to achieve a collateralized lending model closer to native BTC.

What is BTCFi?

BTCFi stands for Bitcoin DeFi, encompassing the lending, stablecoin, yield asset, and on-chain financial ecosystem built around Bitcoin.

Which chain is Zest Protocol built on?

Zest Protocol primarily runs on the Stacks network and connects to the Bitcoin network via Stacks.

Is ZEST a governance token?

ZEST is generally used for governance and incentive purposes within the protocol ecosystem. However, specific tokenomics should be verified with official sources.

What is the difference between Zest Protocol and Aave?

Zest Protocol is designed for the Bitcoin DeFi marketplace, while Aave is built on the Ethereum DeFi ecosystem, with clear differences in asset structure and underlying network.