𝐅𝐄𝐃 𝐑𝐀𝐓𝐄 𝐇𝐈𝐊𝐄 𝐎𝐃𝐃𝐒 🧐

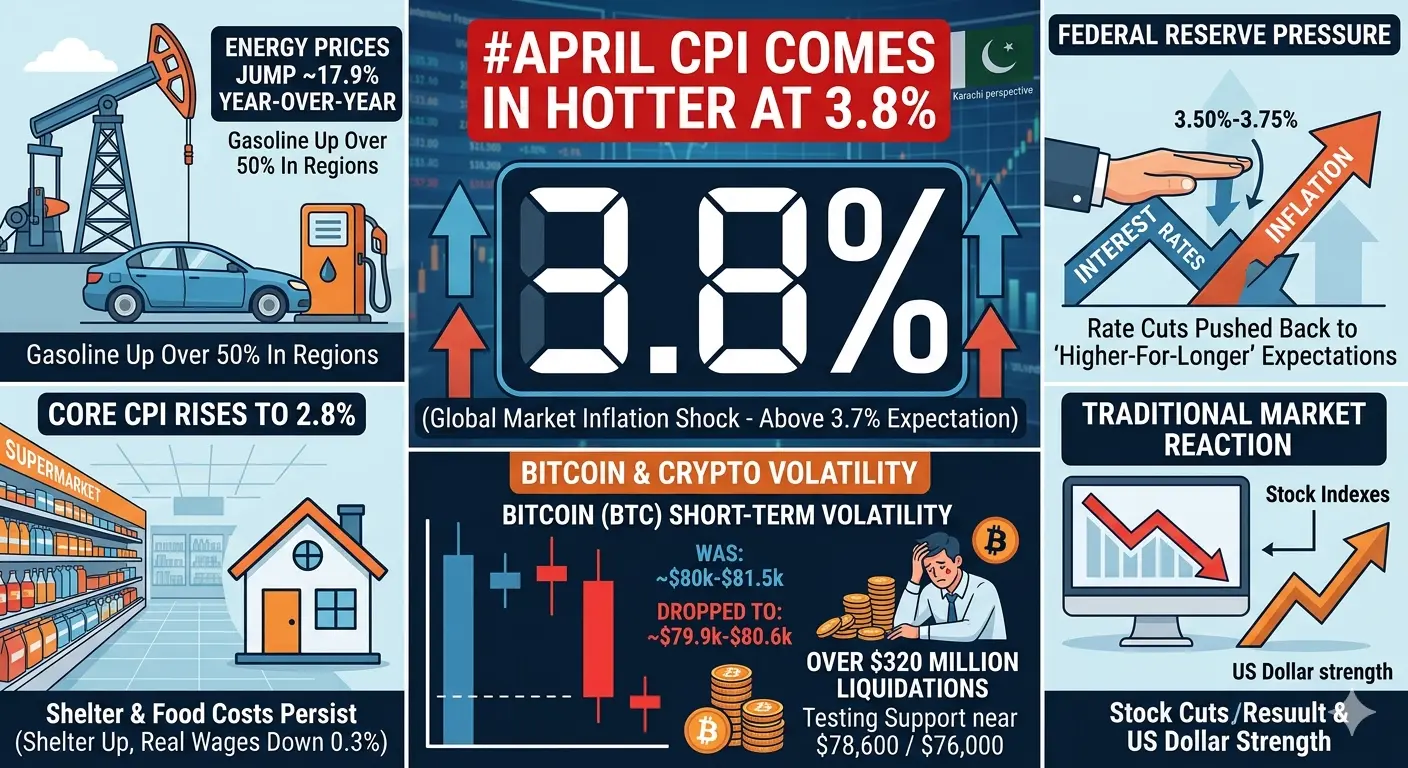

The April CPI print landed hotter than expected and markets are repricing quickly. Headline inflation came in at 3.8% year-on-year, above the 3.7% consensus and the highest reading since May 2023 . Core CPI ticked up to 2.8% against expectations of 2.7% . The immediate result is that rate hike odds for 2026 just hit a new cycle high.

According to CME FedWatch, markets are now pricing a roughly 30% to 31% probability of a rate hike by December 2026 . That is the highest level since the hiking cycle ended. The June meeting is essentially locked at a 98% chance of a hold, but the December probabilities are what signal the genuine shift in sentiment . Rate cuts have been almost entirely priced out for the remainder of the year.

Here is the breakdown of what drove the number. Energy prices accounted for 40% of the monthly CPI increase, with gasoline up 28.4% year-on-year and the broader energy index surging 17.9% . The Iran conflict and the effective closure of the Strait of Hormuz are feeding directly into every transportation-dependent category. Shelter costs jumped 0.6% month-on-month, partly due to a one-time statistical adjustment tied to the October government shutdown that artificially suppressed rent readings last year . That adjustment was expected, but the magnitude still caught attention.

The real wage story adds another layer. Annual inflation-adjusted average hourly wage growth turned negative for the first time since April 2023 . Nominal wages grew roughly 3.6% while prices grew 3.8%, meaning the average American worker lost purchasing power over the past year despite receiving larger paychecks . This is not just a Wall Street concern. It is a kitchen-table issue that will shape political dynamics heading into the November midterms.

The Fed's incoming leadership transition matters here. Kevin Warsh is expected to take over from Powell on May 15. Analysts have already flagged that this CPI print has boxed in the new chair before he even begins, leaving almost no room for dovish signals in his initial communications . The credibility question is front and center. If inflation keeps surprising to the upside during the first months of a new Fed regime, the pressure to act with a hike rather than just holding will intensify.

There is a counterpoint worth acknowledging. Fidelity's research team pointed out that this inflation wave is overwhelmingly supply-driven, tied to energy constraints from the Middle East conflict . Raising interest rates does not produce more oil or reopen shipping lanes. The core driver is geopolitical, not demand-side overheating. The labor market is cooler today than it was during the 2022 inflation spike, wage growth has slowed, and the inflationary pressures have not yet broadened meaningfully beyond energy . This is the argument for why hikes are not inevitable and why the Fed can afford to stay on hold through 2027. Bank of America shares this view, forecasting a hold until the second half of 2027 .

For crypto markets, the implications are mixed and nuanced. A rate hike or even sustained hawkish hold pushes up real yields, which historically acts as a headwind for risk assets including Bitcoin. But the same energy-driven inflation that is eroding real wages and pressuring fiat purchasing power also strengthens the long-term narrative for hard assets with fixed supply. The tension between these two forces is what makes the current macro environment tricky to trade with conviction in either direction.

The next CPI print arrives June 10 and will either validate the rate hike fears or give the Fed room to stay the course. Between now and then, the CLARITY Act markup and the Warsh transition will compete for market attention.

Do you see the 31% rate hike probability as underpriced or overpriced given that this inflation is supply-driven rather than demand-driven? And is the negative real wage data shifting how you think about Bitcoin as a savings vehicle versus simply a risk asset?

This post is for informational purposes only and does not constitute financial advice.

#FederalReserve #CPI #Inflation #Bitcoin

#GateSquareMayTradingShare

The April CPI print landed hotter than expected and markets are repricing quickly. Headline inflation came in at 3.8% year-on-year, above the 3.7% consensus and the highest reading since May 2023 . Core CPI ticked up to 2.8% against expectations of 2.7% . The immediate result is that rate hike odds for 2026 just hit a new cycle high.

According to CME FedWatch, markets are now pricing a roughly 30% to 31% probability of a rate hike by December 2026 . That is the highest level since the hiking cycle ended. The June meeting is essentially locked at a 98% chance of a hold, but the December probabilities are what signal the genuine shift in sentiment . Rate cuts have been almost entirely priced out for the remainder of the year.

Here is the breakdown of what drove the number. Energy prices accounted for 40% of the monthly CPI increase, with gasoline up 28.4% year-on-year and the broader energy index surging 17.9% . The Iran conflict and the effective closure of the Strait of Hormuz are feeding directly into every transportation-dependent category. Shelter costs jumped 0.6% month-on-month, partly due to a one-time statistical adjustment tied to the October government shutdown that artificially suppressed rent readings last year . That adjustment was expected, but the magnitude still caught attention.

The real wage story adds another layer. Annual inflation-adjusted average hourly wage growth turned negative for the first time since April 2023 . Nominal wages grew roughly 3.6% while prices grew 3.8%, meaning the average American worker lost purchasing power over the past year despite receiving larger paychecks . This is not just a Wall Street concern. It is a kitchen-table issue that will shape political dynamics heading into the November midterms.

The Fed's incoming leadership transition matters here. Kevin Warsh is expected to take over from Powell on May 15. Analysts have already flagged that this CPI print has boxed in the new chair before he even begins, leaving almost no room for dovish signals in his initial communications . The credibility question is front and center. If inflation keeps surprising to the upside during the first months of a new Fed regime, the pressure to act with a hike rather than just holding will intensify.

There is a counterpoint worth acknowledging. Fidelity's research team pointed out that this inflation wave is overwhelmingly supply-driven, tied to energy constraints from the Middle East conflict . Raising interest rates does not produce more oil or reopen shipping lanes. The core driver is geopolitical, not demand-side overheating. The labor market is cooler today than it was during the 2022 inflation spike, wage growth has slowed, and the inflationary pressures have not yet broadened meaningfully beyond energy . This is the argument for why hikes are not inevitable and why the Fed can afford to stay on hold through 2027. Bank of America shares this view, forecasting a hold until the second half of 2027 .

For crypto markets, the implications are mixed and nuanced. A rate hike or even sustained hawkish hold pushes up real yields, which historically acts as a headwind for risk assets including Bitcoin. But the same energy-driven inflation that is eroding real wages and pressuring fiat purchasing power also strengthens the long-term narrative for hard assets with fixed supply. The tension between these two forces is what makes the current macro environment tricky to trade with conviction in either direction.

The next CPI print arrives June 10 and will either validate the rate hike fears or give the Fed room to stay the course. Between now and then, the CLARITY Act markup and the Warsh transition will compete for market attention.

Do you see the 31% rate hike probability as underpriced or overpriced given that this inflation is supply-driven rather than demand-driven? And is the negative real wage data shifting how you think about Bitcoin as a savings vehicle versus simply a risk asset?

This post is for informational purposes only and does not constitute financial advice.

#FederalReserve #CPI #Inflation #Bitcoin

#GateSquareMayTradingShare